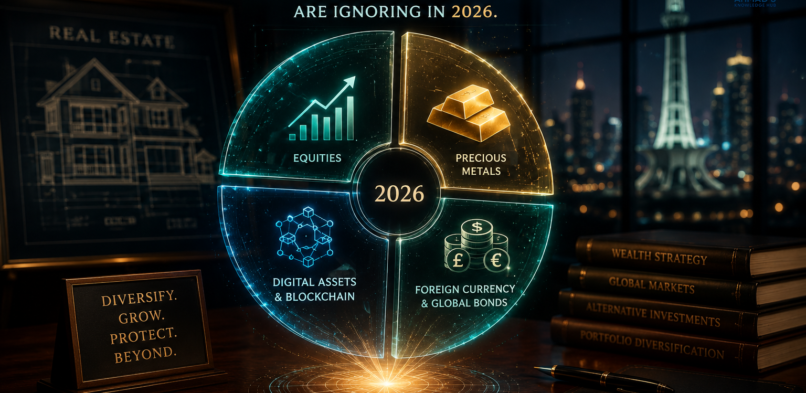

If you ask the average Pakistani where to invest a surplus of cash, the answer is almost reflexive: “Zameen” (Land).

For decades, buying a plot in a housing society or hoarding real estate “files” has been the undisputed champion of wealth preservation in Pakistan. And for a long time, it worked. But as we navigate the economic realities of 2026, characterized by shifting tax regimes on non-utilized land, rising holding costs, and a rapidly digitizing economy, the old playbook is showing its cracks.

Real estate is highly illiquid, capital-intensive, and increasingly heavily taxed. If your entire net worth is locked in brick-and-mortar, you are not diversified; you are trapped. To build robust, inflation-proof wealth in 2026, Pakistani investors need to look beyond the plot. Here are five powerful asset classes that are currently being ignored by the masses.

1. Shariah-Compliant Mutual Funds (The Power of Compound Liquidity)

Many Pakistanis still leave their savings in regular checking accounts, allowing inflation to silently erode their purchasing power day by day. In 2026, the barrier to entry for Mutual Funds is lower than ever. Through digital applications, investors can park their capital in Islamic Income Funds or Money Market Funds. These funds invest in highly secure, short-term instruments (like government Sukuks) and offer competitive annualized returns.

- The Advantage: Unlike a plot of land, which takes months to sell, mutual funds offer high liquidity. You can withdraw your money within 24 to 48 hours while earning daily compounding profit.

2. Digital Gold and Gold-Backed Securities

Gold is deeply embedded in South Asian culture, but physical gold comes with severe drawbacks: making charges (which you lose upon resale), locker fees, and constant security risks. The modern investor is turning to Digital Gold and Gold Exchange Traded Funds (ETFs) available through the Pakistan Stock Exchange (PSX) or specialized fintech apps.

- The Advantage: You get the same inflation-hedging benefits of physical gold, protecting you against Rupee depreciation, but with zero storage risk and instant liquidity. You can buy fractions of a gram with a single tap on your smartphone.

3. Global Equities (Through Fractional Investing)

A major flaw in the traditional Pakistani portfolio is 100% exposure to the domestic economy. If the local market dips, your entire net worth dips. With the rise of modern brokerage apps operating in Pakistan, retail investors can now buy fractional shares of global giants or Shariah-compliant international index funds. You don’t need $3,000 to buy a share of a major tech company; you can invest $10.

- The Advantage: Geographic and currency diversification. By holding assets priced in foreign currencies, you create a natural shield against local economic turbulence.

4. The PSX Dividend Aristocrats

The Pakistan Stock Exchange (PSX) often scares away the average investor because it is viewed as a “casino.” This is a misconception born from a lack of financial literacy. While day-trading is risky, value investing is not. Pakistan has several “Dividend Aristocrats”, which are the companies in the fertilizer, power, and banking sectors that have consistently paid high, reliable dividend yields year after year, regardless of political noise.

- The Advantage: Cash flow. While real estate sits empty waiting for capital appreciation, dividend-paying stocks put cash directly into your bank account every quarter, creating a passive income stream.

5. Intellectual Capital (The Iqbalian Asset)

As we discuss frequently on Ahmad’s Knowledge Hub, the ultimate driver of the economy is the human mind. Allama Iqbal’s concept of Khudi (Selfhood) applies directly to personal finance. In the era of Agentic AI and global digital labor, your most appreciating asset is not in a bank; it is your skill set. Investing in high-level certifications, specialized coaching, or building a personal digital brand yields an ROI that no financial instrument can match.

- The Advantage: Stocks can crash, and real estate bubbles can burst, but intellectual capital is theft-proof and infinitely scalable.

Conclusion: Rebuilding the Portfolio

Owning a home is a fundamental goal, and real estate will always have a place in a mature portfolio. But it should be a pillar of your wealth, not the entire foundation. In 2026, the tools for global diversification, instant liquidity, and compounding growth are sitting in your pocket. The era of the “one-asset portfolio” is over. It is time to diversify.

Related Articles:

Leave a comment